The European Central Bank has cautioned that the rapid rise of stablecoins could weaken bank lending and complicate the transmission of monetary policy across the euro area. In a new working paper titled “Stablecoins and Monetary Policy Transmission,” the ECB said growing use of these digital assets may lead households and firms to shift money away from traditional bank deposits, reducing banks’ ability to extend credit.

Stablecoins are digital tokens typically pegged to fiat currencies such as the US dollar or the euro. While they are designed to maintain stable value, their expanding role in payments and savings is raising fresh questions for policymakers in Europe.

Deposit Shift Could Squeeze Bank Lending

According to ECB staff, rising interest in stablecoins is already linked to a measurable decline in retail bank deposits and a reduction in lending to firms. The study highlights what it calls a deposit substitution effect, where customers move funds from bank accounts into digital tokens.

Banks depend heavily on deposits as a stable and relatively low cost source of funding. These deposits support loans to households and businesses. If deposits fall, banks may have to turn to wholesale or market based funding, which is often more expensive and less predictable. That shift could tighten credit conditions for companies and consumers.

The ECB noted that reduced deposits can ultimately shrink the amount of credit available to the real economy. This, in turn, may slow investment and growth, especially if stablecoin adoption accelerates.

Implications for Monetary Policy Transmission

Beyond bank funding, the central bank warned that stablecoins could interfere with how interest rate decisions flow through the financial system. Monetary policy typically works by influencing banks’ funding costs and lending rates. If deposits decline or funding structures change, the relationship between policy rates and lending conditions may weaken.

The ECB paper found that stablecoin adoption can affect multiple channels of monetary policy transmission. The scale of the impact depends on how widely stablecoins are used, how they are structured and how they are regulated.

In cases of high adoption, the link between central bank rate changes and bank lending could become less predictable. That uncertainty may complicate efforts to control inflation or support growth during economic slowdowns.

Scale and Design Make a Difference

The report emphasized that the effects are not uniform. They vary depending on the size of the stablecoin market and the specific design features of the tokens. For example, stablecoins that offer interest or are easily convertible into bank deposits may have different implications compared to those used primarily for payments.

Regulation also plays a critical role. Clear rules on reserves, transparency and redemption rights can influence how attractive stablecoins are relative to traditional deposits. The ECB has been closely monitoring developments in this area as part of its broader efforts to assess financial stability risks.

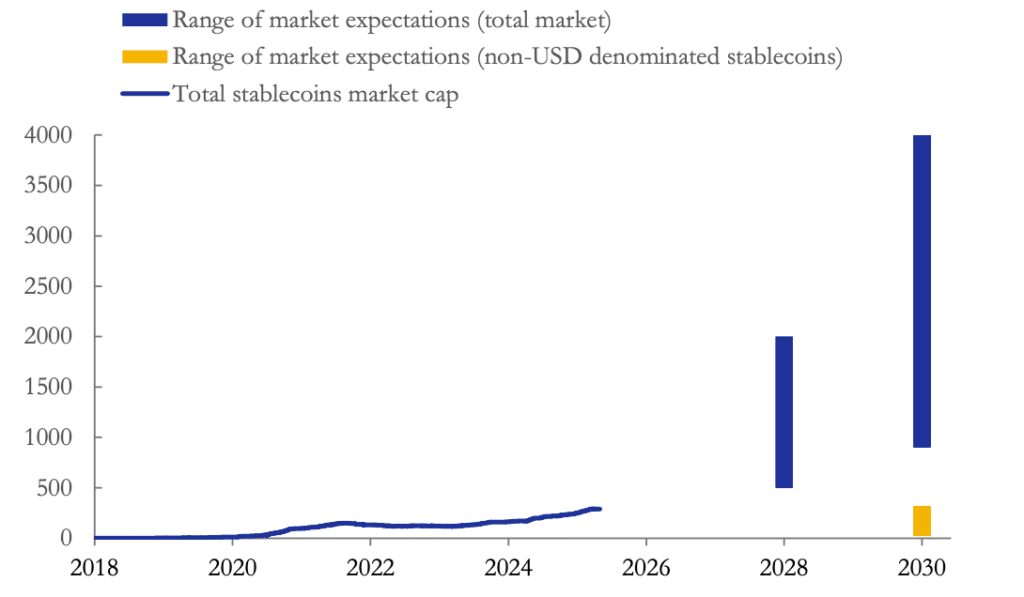

Stablecoins have expanded rapidly in recent years. Their combined market capitalization has more than doubled over the past three years and now stands at about 312 billion dollars. Projections suggest the market could grow to as much as 2 trillion dollars by 2028.

Dollar Dominance Raises Sovereignty Concerns

A key concern for the euro area is the dominance of dollar backed stablecoins. Data cited in the working paper and from market sources show that tokens pegged to the US dollar account for the overwhelming majority of the global stablecoin market. At present, dollar linked stablecoins are valued at roughly 301 billion dollars, representing about 97 percent of total market capitalization.

The ECB warned that widespread use of foreign currency stablecoins could further weaken the connection between domestic monetary policy and bank lending. If euro area residents increasingly hold and transact in dollar denominated tokens, the influence of euro interest rate decisions may diminish.

ECB officials have previously raised concerns that the growing reach of dollar stablecoins could affect monetary sovereignty and the euro’s role in cross border payments. A market dominated by non euro tokens may amplify these risks.

Ongoing Monitoring by the ECB

The working paper forms part of the ECB’s broader research into digital assets and their implications for financial stability. While stablecoins offer potential benefits such as faster payments and new financial services, the central bank is examining how their growth could reshape funding structures within the banking system.

For now, the ECB’s findings suggest that policymakers will need to factor stablecoin adoption into their assessment of monetary conditions. As digital assets continue to evolve, their interaction with traditional finance is likely to remain under close scrutiny in Frankfurt.