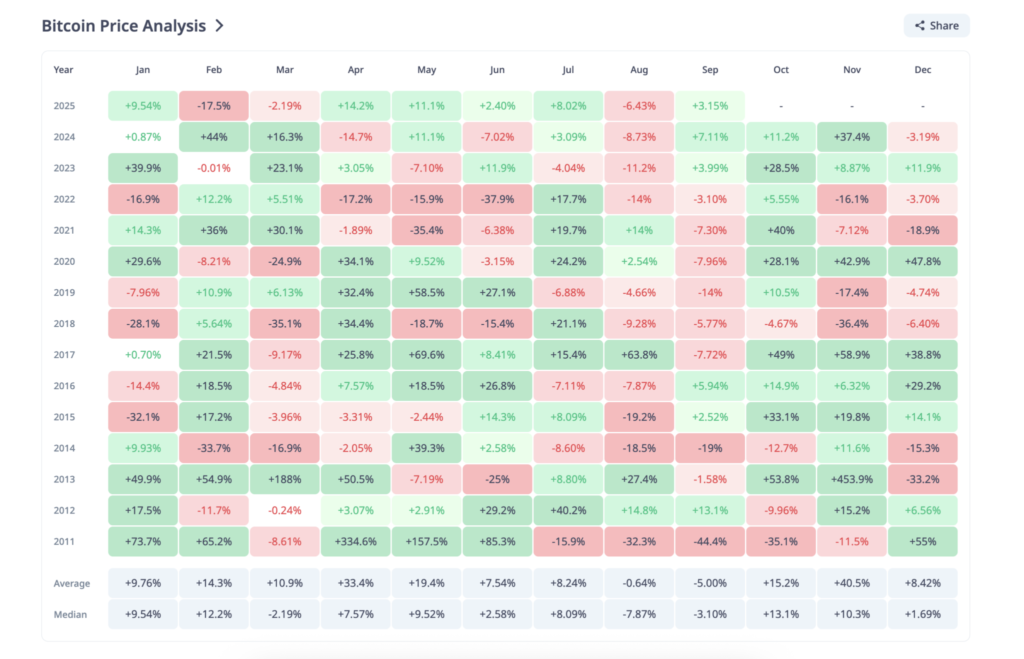

For over a decade, September has been the most dreaded month in crypto markets. Historically, both Bitcoin and Ethereum have suffered brutal drawdowns in this period, with losses so consistent that traders coined the phrase “crypto September blues.” Yet in 2025, the setup feels markedly different. With thinner exchange reserves, spot ETFs absorbing selling pressure, record stablecoin balances, and growing institutional adoption, this month may finally mark the end of September’s dark legacy.

A Decade of Pain: Why September Has Been Crypto’s Weakest Month

Since 2013, Bitcoin has posted a median September return of –3.1%, while Ethereum has fared even worse with –12.7%. Historic collapses, such as Bitcoin’s –19% in 2014 and Ethereum’s –21% in 2017, cemented September’s reputation as the weakest month for digital assets.

Some of the most notable setbacks include:

- 2014: Bitcoin slumped 19%.

- 2015: Ethereum recorded its worst-ever September, plunging 45%.

- 2019: Bitcoin fell 14%, while Ethereum barely managed a 3.95% gain.

- 2022: Bitcoin and Ethereum lost 3.1% and 14.6% respectively, battered by tightening global liquidity.

Even during bullish cycles, September had a knack for derailing momentum. Market structure, macroeconomic cycles, and sentiment converged to create an environment ripe for panic selling. Exchange reserves were historically high, meaning ample supply ready to hit the market. Profit-taking was limited, leaving fewer holders in profit and more susceptible to fear-driven liquidations.

In 2024, however, a rare shift occurred. Bitcoin posted a 7.1% gain and Ethereum rose 3.2%, helped by the launch of ETFs and a timely 50-basis-point rate cut by the US Federal Reserve. This proved that the so-called curse could bend under the weight of new structural forces.

Now, in September 2025, Bitcoin and Ethereum both hover near all-time highs, and the question is whether this month could finally deliver a historic break in trend.

Leaner Exchanges, Stronger Demand

The single most striking change from past Septembers lies in exchange reserves. Historically, these reserves were bloated, meaning ample supply available to sell whenever sentiment soured. Today, the picture looks very different.

- Bitcoin exchange reserves have dropped from around 3.0 million BTC in September 2024 to just 2.4 million BTC today.

- Ethereum reserves have declined from 19.3 million ETH to 17.3 million ETH in the same period.

This thinning supply suggests that fewer coins are sitting on exchanges waiting to be dumped. Instead, whales and long-term holders have been accumulating, with evidence that September buying already began before the month even opened.

Adding further support are the ETFs, which now act as structural demand absorbers. Since launch, Bitcoin ETFs have attracted lifetime inflows of $54.58 billion, including $332.76 million so far in September alone. Ethereum ETFs are not far behind, with $13.49 billion in lifetime inflows.

Unlike in earlier cycles, ETFs serve as steady, institutional-grade buyers capable of soaking up selling pressure. This dynamic simply did not exist when September sell-offs became infamous.

Stablecoins and Institutional Firepower

Another decisive difference in 2025 is the scale of stablecoin reserves. Stablecoins represent dry powder for re-entry into the market, and their balances have nearly doubled year-on-year:

- September 2024: $28.4 billion.

- September 2025: $54.9 billion.

This means vast liquidity is already on-chain, ready to deploy should prices dip. In past Septembers, a lack of immediate capital often exacerbated sell-offs.

Institutional adoption is also reshaping the market landscape. Public companies now hold significant treasuries in both Bitcoin and Ethereum:

- The top 100 public Bitcoin holders, led by MicroStrategy, collectively own 998,613 BTC.

- On Ethereum, Sharplink Gaming disclosed holdings of 837,230 ETH as of August 31, while others such as Bitmine continue to accumulate.

This wave of institutional demand acts as a buffer. Unlike retail traders, these entities are less prone to panic and more likely to buy dips. While Bitcoin has enjoyed institutional support for several cycles, Ethereum’s adoption at this scale is relatively new and represents a fresh dynamic heading into September 2025.

The Risks That Linger

Despite these structural supports, September is not without risks. The most pressing include high profit supply, weakening self-custody conviction, and macroeconomic headwinds.

Currently, the proportion of coins in profit is unusually high:

- Bitcoin in profit: up from 73.8% in September 2024 to 90.1% today.

- Ethereum in profit: up from 69.9% to 95.9%.

With so many holders in the green, there is always the temptation to take profit, especially in a month with a historically bearish bias. Yet ETFs and corporate treasuries could absorb outflows more effectively than in past years.

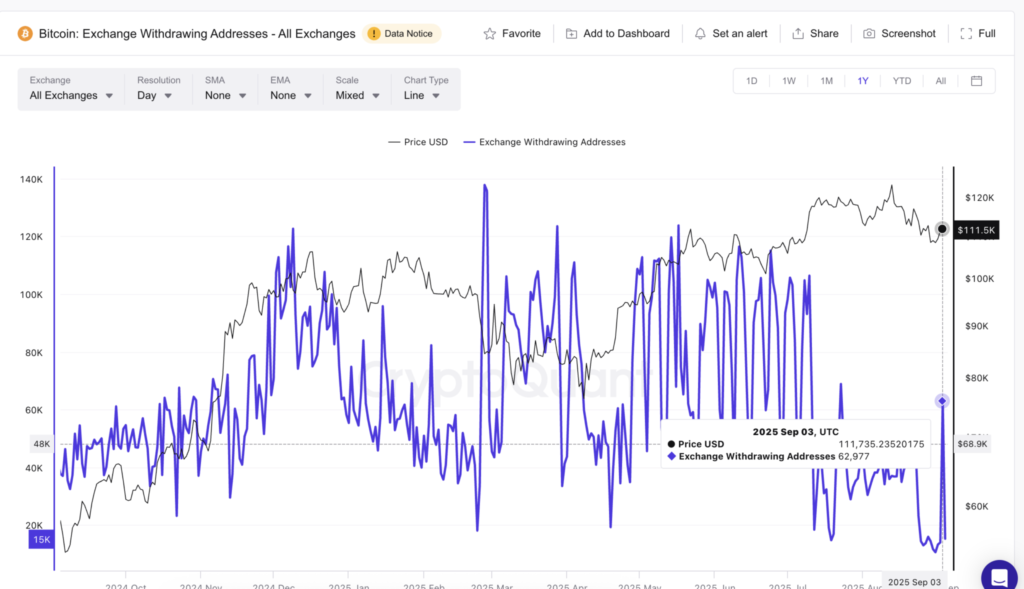

Self-custody signals are less encouraging. Bitcoin withdrawal addresses fell from 37,745 in September 2024 to just 15,241 today, suggesting weaker conviction. However, a recent spike to 62,977 withdrawal addresses on September 3 indicates that dip-buyers remain active.

Macro conditions also present challenges. The US 10-year Treasury yield at 4.22% implies elevated borrowing costs and reduced appetite for risk assets. Gold’s rise to record highs signals investors’ preference for safety. Analysts at Bitfinex recently noted that Bitcoin is down 13% from its recent peak, with summer retracements weighing on sentiment.

However, the Federal Reserve is widely expected to cut rates this month. The last time it did so in September 2024, Bitcoin enjoyed strong ETF inflows and posted positive returns. If repeated, this could provide the catalyst that flips sentiment.

Could 2025 Be the Year the Curse Breaks?

For over a decade, September has haunted crypto investors, synonymous with sell-offs and lost momentum. But 2025 looks materially different. Exchange reserves are leaner, ETF demand has already exceeded $68 billion, stablecoin liquidity has doubled, and institutions are actively buying dips.

Yes, risks remain. High profit supply and elevated yields could still trigger bouts of volatility. Yet, the difference this year is the strength of mitigating forces from ETFs to corporate treasuries, that were largely absent in earlier cycles.

For now, the market watches closely. If the curse is finally broken, September 2025 will not be remembered for blues, but for green candles and a turning point in crypto history.